05 Aug 2025

Global banking is going through a seismic shift, a profound transformation if I may call it, led by inventive mobile technology. With the number of global mobile banking users set to surpass 3.5 billion users, these are now the primary interfaces redefining the customer experience for financial institutions.

Fueled by the willingness of customers and evolution of user expectations worldwide, approximately 66% of the world’s population now has access to mobile banking. Coupled with the competitive nature of the banking sector, banks are constantly encouraging the use of mobile apps to provide a 360 degrees experience to their customers. Mobile payments now account for 49% of all digital banking transactions, while 76% of adults use mobile banking apps daily.

As traditional bank branch visits decline, with a 51% decline recorded in the US alone in 2025, mobile banking transactions record a sharp rise with 67% increase in the US in 2025.

Our article discusses how banks are leveraging mobile banking app development for hyper-personalized features, clear app layouts, thoughtful design, AI, expense tracking features, categorizations, goal setting, bill reminders, and much more to redefine the customer experience.

Customers today approach their financial institutions with exceptionally high expectations. Often comparing their digital banking experience not just to other financial providers, but to leading technology platforms across various industries.

This phenomenon, where consumer-grade digital experiences set the benchmark for enterprise services, means that the personalized interactions offered by e-commerce giants or streaming services are now the standard for financial applications.

A significant majority of customers, between 50% and 70%, now prefer digital channels due to their inherent convenience and constant availability. This preference is reflected in high satisfaction levels, with 96% of consumers expressing contentment with their mobile and online banking experiences.

Beyond basic satisfaction, a deeper demand exists.

62% of digital banking customers prioritize “instant access to help” over traditional factors like interest rates or account features, underscoring a critical need for immediate issue resolution. A substantial 66% of consumers also expect companies to understand their unique needs, and 52% anticipate personalized offers.

The stakes are considerable in this evolving environment, as approximately 80% of consumers would consider switching banks after experiencing more than one negative interaction. This indicates that while basic digital services are now expected, the quality of the customer experience has become the primary differentiator.

Products and services are increasingly interchangeable, making the overall experience the most sustainable competitive advantage in banking. This reality necessitates that investment in mobile banking app development shifts from merely adding features to intelligently reimagining the entire customer journey, prioritizing seamless user experience, proactive support, and hyper-personalization to foster loyalty and drive long-term revenue.

The data unequivocally points to a mobile-first approach in banking.

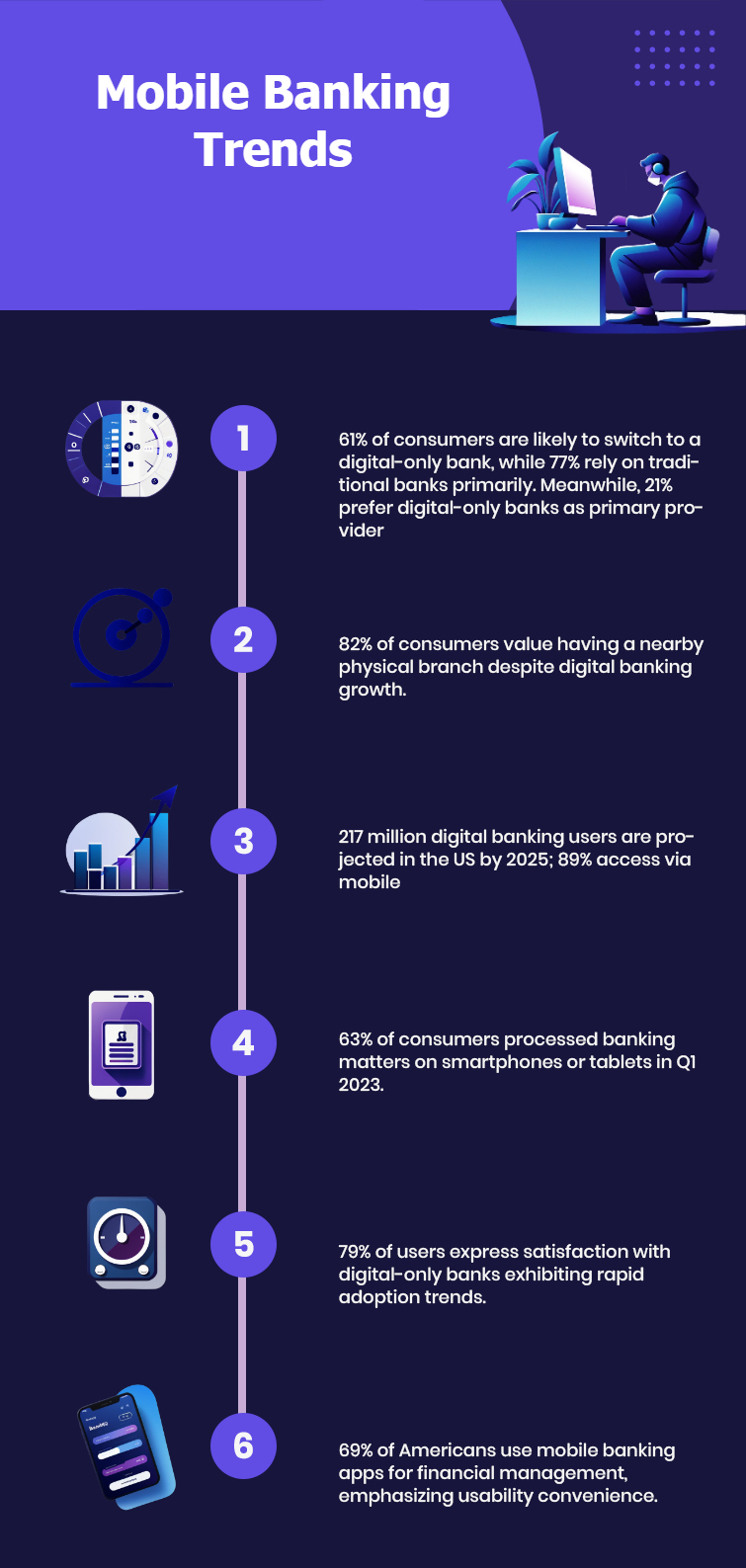

A majority of U.S. consumers, 55%, now use mobile apps as their primary method for managing bank accounts, marking the highest percentage recorded since 2017. This preference for mobile extends across generations, with 68% of Millennials and 64% of Gen Z primarily relying on mobile banking apps.

Indeed, mobile preference exceeds 50% for all age groups except Baby Boomers. Globally, mobile banking transactions now account for 62% of all banking activities, a significant increase from 35% in 2018. This widespread adoption is driven by tangible benefits. Consumers report saving an average of 1.8 hours monthly by using mobile banking apps instead of visiting physical branches.

Despite this profound digital acceleration, physical branches are demonstrating surprising resilience. A notable 72% of customers still plan to use their nearby branch at a similar frequency, and 38% consider branches indispensable, particularly for complex advice or during times of financial uncertainty. This suggests a nuanced evolution rather than a complete replacement.

The role of branches is transitioning from transactional hubs to advisory centers, focusing on high-value interactions and relationship building, while mobile apps efficiently handle routine, self-service tasks. This convergence of digital and physical channels, often termed “phygital” banking, requires a sophisticated omnichannel strategy.

Customer delight in the digital age extends far beyond basic functionality. It is about creating an emotionally resonant and genuinely engaging experience.

Fintechs and neobanks are leading this transformation by introducing concepts like “Dopamine Banking,” which integrates finance with emotions and entertainment to foster engaging and rewarding digital interactions. This approach aims to address the common perception of traditional banking’s digital services as boring and uninspiring.

Dopamine banking leverages insights from neuroscience and neuromarketing, employing eye-catching interface designs, gamification, reward programs, and community-building initiatives to establish deeper connections with customers. This involves using bold colors, fonts, patterns, micro-interactions, and even haptic feedback to trigger the brain’s reward system.

Small, positive micro-experiences, such as receiving personalized tips, viewing attractive dashboards that track financial health, contribute to positive associations with money management.

Gamified solutions, which 90% of users find highly effective, are particularly instrumental in enhancing loyalty and engagement. This emphasis on emotional connection is a powerful driver of customer loyalty, leading to increased retention and spending.

As financial institutions increasingly leverage psychological principles in their app design. There is a growing responsibility to ensure these techniques promote healthy money habits without inadvertently triggering impulsive purchasing behaviors. This ethical consideration influences how mobile banking app development services are delivered and audited.

The core pillars of modern banking app customer experience are unparalleled convenience and accessibility, liberating users from traditional banking constraints.

The expectation for 24/7, on-demand banking has become a fundamental requirement for today’s consumers. Customers now desire immediate assistance for their financial queries, expecting chatbots or agents to resolve simple issues instantly without the frustration of queues, lags, or lengthy email response times.

A 2025 Celent survey underscored this imperative, indicating that 62% of digital banking customers prioritize “instant access to help” over traditional considerations like interest rates or account features.

Mobile banking apps are the primary enablers of this “always-on” service model. They are providing convenient access to accounts anytime, from virtually anywhere. Digital-only banks, unburdened by legacy systems, particularly excel in this area, achieving continuous 24/7 support through sophisticated automated triaging, smart escalation protocols, and advanced AI orchestration.

This transformation reflects the broader “always-on” nature of modern life, where consumers expect services to be available at their convenience. Consequently, banks must invest in robust, scalable backend systems and cloud infrastructure to support these continuous operations.

Mobile banking apps have fundamentally liberated customers from the geographical and temporal constraints of traditional banking. This empowers customers to manage their finances entirely through their smartphones, thereby eliminating the need for physical branch visits. Mobile banking transactions now constitute 62% of all banking transactions globally, a substantial increase from 35% in 2018.

This significant shift is driven by tangible efficiency gains. The average mobile transaction takes just 1 minute and 27 seconds to complete, representing an impressive 82% reduction in time compared to performing the same transaction in a physical branch. Overall, consumers report saving an average of 1.8 hours monthly by opting for mobile banking apps.

This pervasive adoption demonstrates that mobile devices are no longer merely a way to bank, but increasingly the primary way for many consumers to manage their financial lives. This elevates the importance of the mobile banking app development experience to the central point of a customer’s financial interactions.

An intuitive User Interface (UX/UI) is paramount for enhancing user experience and fostering customer loyalty. Conversely, a poorly designed interface can have significant repercussions, with poor aesthetics leading to 52% of existing users not returning to a digital platform.

Core elements of a positive UX include frictionless transactions, such as one-click payments, quick transfers, and real-time transaction updates. Digital-only banks exemplify this by driving their UX decisions with behavioral analytics and design thinking, rather than being constrained by internal processes or legacy systems.

A user-centric UI/UX is not merely an aesthetic choice. It is crucial for financial interactions, as it enhances brand value, improves security, boosts profitability, and promotes financial inclusion. Simplicity, flexibility, consistency, engaging micro-interactions, and empathy-driven design are key trends in achieving this effortless user experience.

Beyond aesthetics, a thoughtful design can actively guide users towards secure behaviors, such as adopting strong passwords and two-factor authentication. This implies that good UX can effectively reduce the human error component of security breaches, making it a critical component of a comprehensive security strategy for banking apps.

Additionally, the significant customer churn associated with poor aesthetics (52% of users not returning) directly translates to lost revenue and increased operational costs due to higher customer support queries. While a premium UX/UI might increase the initial banking app development cost, the long-term benefits in terms of customer retention, reduced support overheads, and enhanced brand reputation outweigh these expenses.

The evolution of mobile banking app development is moving beyond mere transactional capabilities to offer deeply personalized experiences, transforming banks into proactive financial partners.

Artificial Intelligence (AI) and Machine Learning (ML) are pivotal in delivering highly personalized customer experiences. Banks are increasingly leveraging data-driven insights to proactively deliver hyperpersonalized content, offers, and support to individual customers.

AI provides personalized financial guidance based on spending habits, offers real-time customized financial products like credit line increases or custom loan options. AI analyzes user behavior, habits, and preferences to offer insights and recommendations.

A prime example of this capability is Bank of America’s AI virtual assistant, Erica, which handled over 2 billion interactions in 2024, answering more than 98% of inquiries within 44 seconds. AI-powered virtual assistants can offer financial advice based on individual income, spending habits, and financial goals , and even automate payments, track due dates, and identify savings opportunities. Significantly, 75% of consumers find their banks’ use of AI to understand their needs and preferences to be acceptable.

This capability for AI to anticipate customer needs and proactively offer relevant products and services fundamentally shifts the banking service model. Instead of merely responding to customer queries, banks can predict and address financial needs before they even arise.

This necessitates a significant investment in robust data analytics platforms and advanced AI models as part of the mobile banking app development strategy. This moves banks beyond basic reporting to predictive capabilities.

AI-powered financial coaches and virtual assistants make sophisticated financial planning tools and advice. Historically these were accessible only through human financial advisors, and are now available to a much broader audience. This widespread access could lead to increased financial literacy and improved financial health across populations, potentially narrowing economic disparities.

For banking app developers, this means focusing on building intuitive AI interfaces that simplify complex financial concepts and empower users to make informed decisions, ensuring the technology serves a broader societal good.

Hyper-personalization involves personalizing every aspect of the banking experience to the individual.

Revolut uses AI to suggest financial products based on monthly activity. Monzo provides real-time alerts for unusual transactions. AI-powered tools that personalize financial product recommendations have demonstrated a significant impact, leading to a 5x increase in click-through rates for personalized offers.

This level of personalization directly contributes to increased customer satisfaction, retention, loyalty, and revenue. Modern customers now expect the ability to personalize their dashboards and quick links , and hyper-personalization can increase engagement by up to 38%. Companies like Personetics exemplify this by analyzing transaction data in real-time using machine learning to categorize purchasing behavior for personalized suggestions.

Fintechs are innovatively blending education, entertainment, and lifestyle perks through gamification to make financial management more engaging and accessible.

Gamified solutions are proving highly effective, with 90% of users finding them engaging, which significantly enhances loyalty and engagement. Apps like Buddy utilize colorful charts, budget streaks, and progress tracking to motivate users towards their financial goals. Similarly, Cleo makes budgeting engaging and intuitive with witty reminders and AI-powered insights, transforming a mundane task into an interactive experience.

Gamification can celebrate small victories and provide financial health scores, subtly encouraging positive financial habits. Banking apps are increasingly incorporating learning resources, and users who actively engage with these educational modules report 28% higher savings rates.

This application of gamification in banking apps is a sophisticated use of behavioral economics. By providing small boosts of dopamine for positive financial actions. These can be like reaching a savings goal or maintaining a budget streak. Apps can subtly yet effectively nudge users towards healthier financial habits. This direct correlation with higher savings rates validates its efficacy.

For banking app developers, this means integrating psychological principles into design, focusing on clear progress visualization, positive reinforcement, and goal-setting mechanisms to drive desired user behaviors and foster greater financial literacy.

Today, where sensitive financial data is constantly exchanged, trust and security are critical. Mobile banking app development must prioritize robust security measures while simultaneously maintaining a seamless user experience.

Biometric authentication has emerged as a cornerstone of modern banking app security. Banks build customer confidence by implementing biometrics, alongside encryption and real-time fraud alerts.

The integration of the latest biometric identification methods like fingerprint, facial, voice, and iris recognition provides more secure and convenient access. This technology effectively eliminates the need for cumbersome passwords and security questions, streamlining the authentication process.

Digital-only banks, in particular, leverage biometric logins as a key feature to build trust with their user base. Expert opinion complements the importance of this technology, asserting that biometric authentication is mandatory and that a compromised password alone should never grant access to an account.

Biometric authentication is not merely about enhancing security; it is about making security easier and more intuitive for the user. Traditional security methods, such as complex passwords, often create friction and user frustration, which can lead to poor security hygiene.

By contrast, biometrics offer robust security, making the securest option the most effortless choice for users. This encourages widespread adoption of stronger security practices, thereby enhancing both the security of the application and overall user satisfaction.

Proactive security measures, particularly through real-time fraud alerts, are vital for building and maintaining customer trust.

Banks instill confidence by providing these immediate alerts, which empower customers to stay safe. AI-driven cybersecurity systems continuously monitor transactions and suspicious activities, enabling real-time fraud mitigation and rapid response.

For instance, if a customer typically spends $2,000 per month and a sudden $10,000 transaction appears on their account, AI can immediately trigger an alert before the transaction is processed, allowing the customer to verify or flag it.

Chatbots can also play a crucial role by instantly alerting customers to verify transactions or report potential fraud. In addition, features like transaction confirmation via the app provide real-time notifications and require in-app confirmation, ensuring account holders are aware of all activity and can quickly report any unauthorized transactions. Capital One’s Eno, for example, actively monitors transactions and alerts users to suspicious behaviors, such as duplicate charges or unusually large tips.

This shift to real-time fraud alerts and proactive security represents a fundamental change from merely recovering from fraud to actively preventing it. AI’s ability to analyze spending patterns and flag anomalies empowers customers to become active participants in their own financial security.

This transforms the dynamic from the bank solely being responsible for security to a collaborative, shared responsibility model, where the banking app acts as a vigilant partner.

Consequently, mobile banking app development must incorporate clear, actionable real-time notifications and user-friendly interfaces for reporting suspicious activity. This also implies a need for ongoing customer education on how to interpret and respond to these alerts effectively, fostering a more secure and informed user base.

Beyond robust technical security measures, transparency and data privacy are crucial for cultivating and maintaining customer confidence. Banks must skillfully balance stringent security measures with a low-friction login and approval process to provide both speed and peace of mind.

In an era of increasing data awareness, customers increasingly want to understand how a business is utilizing their data. A significant 69% of users indicate that they consider firms trustworthy if those firms are transparent about their data usage practices.

A thoughtfully designed user experience in banking apps not only helps customers adopt essential security practices but also provides clear information about how their data is being used. Adhering to privacy by design principles is essential for protecting user data and ensuring app development compliance with critical data protection regulations like GDPR or CCPA.

The modern banking experience is characterized by seamless integration, extending beyond the confines of a single app to encompass a holistic omnichannel journey. This requires highly professional banking app development services.

Modern banking apps are evolving from standalone tools into central hubs within a broader financial ecosystem.

This involves integration with digital wallets , various third-party fintech services, and even non-financial super-apps. This interconnectedness, often referred to as embedded finance, is experiencing significant growth, with 72% of surveyed individuals expecting a majority of financial products to be delivered in this integrated manner.

Asian applications like Singapore’s Grab and Indonesia’s Gojek exemplify this trend by integrating e-commerce, rewards, travel booking, and on-demand services into comprehensive lifestyle platforms. This trend is already impacting consumer behavior, with 38% of consumers having accessed financial services through non-banking platforms in 2023.

The ability to integrate with third-party services and create one-stop shops fundamentally relies on open banking principles and robust API infrastructure. APIs and open banking allow financial institutions to offer advanced technological solutions without requiring costly and challenging complete restructures of legacy systems. This implies that banking is moving from a standalone activity to an invisible, seamless layer within a customer’s broader digital lifestyle.

Customers demand a unified and consistent experience across all communication channels. This requires ensuring seamless transitions between in-app chat, AI-powered chatbots, and human agents, with full context maintained.

Banks are actively responding to this demand by embedding 24/7 live chat, AI triage bots, and callback scheduling directly into their banking apps. AI-powered chatbots have evolved significantly. They are now capable of handling complex tasks such as Know Your Customer (KYC) verifications, grievance settlements, advanced inquiries, and even providing financial advice at scale.

UBank in Australia, for instance, utilizes an IBM Watson-driven digital assistant named Mia, which efficiently handles 90% of service inquiries without human intervention. While 70% of banks currently offer chatbots, a substantial 67% of those provide live chat support if the chatbot fails to answer a question after two attempts. Generative AI is further enhancing chatbot responsiveness and resolution accuracy, directly addressing the 61% of bank customers who previously contacted agents due to poor chatbot resolutions.

The ideal customer experience is an omnichannel one, where physical and digital channels seamlessly complement each other.

This omni-channel flow allows customers to initiate a transaction on their mobile banking app and complete it in-branch without the need to re-enter information.. Consistency between online and mobile banking experiences enhances familiarity and overall customer satisfaction. While consumers increasingly expect online self-service, they still desire access to a human when needed.

Physical branches continue to play a crucial role in maintaining customer trust. This is particularly crucial during times of financial insecurity or for complex advisory needs. Banks are strategically integrating digital tools to equip relationship managers with real-time customer insights. This results in better financial advice and is transforming branches into advisory hubs that combine digital tools with personalized consultations.

The future of banking lies in a “phygital” strategy, optimizing the synergy between the two. This means mobile banking app development should not only provide robust digital services but also facilitate seamless handoffs and data sharing with human advisors and physical branches.

The banking app development cost varies significantly, typically ranging from $30,000 to $300,000+, depending on complexity, features, and the development team’s location. Basic applications with standard features lean towards the lower end. Complex, custom-built solutions with advanced security and extensive functionalities can reach the higher end.

Leading factors influencing the mobile banking app development cost include:

MyTeams is a leading banking & fintech app development company, dedicated to building secure, scalable, and user-centric financial solutions that redefine customer experience.

Banking apps have revolutionized customer experience, transforming traditional banking into a seamless, personalized, and always-on digital journey.

Driven by evolving consumer expectations and advancements in mobile banking app development. These applications offer unmatched convenience, hyper-personalized financial guidance through AI, and robust security measures.

The future of banking lies in integrated, omnichannel experiences, where AI augments human interaction and services are embedded into daily life. For financial institutions, investing in expert banking app development is no longer optional but essential for building trust, fostering loyalty, and securing a competitive edge in this rapidly evolving digital landscape.

The Future of Banking: How Digital Transformation Enhances… — perspective.orange-business.com

Nine Best Practices As Banks’ Online and App Customer Experience Evolves — thefinancialbrand.com

How Digital-Only Banks Are Redefining Customer Service — fintecbuzz.com

How Mobile Apps Are Changing the Banking Industry — netguru.com

Redefining Customer Experience in Banking — vacuumlabs.com

Dopamine Banking: How Fintechs Redefine Customer Experience — theuxda.com

Key Customer Experience Trends in Banking — reddit.com

How Fintech Companies Are Revolutionizing Customer Service — kommunicate.io

How Banks Use Mobile Apps to Improve Digital Customer Service — teaminternational.com

Future of Banking: AI, Lifestyle Accounts, Super-Apps, and More — designit.com

6 Most Important Customer Experience Trends in Banking — unblu.com

Consumer Survey Banking Methods 2024 — aba.com

Use Analytics for Retail Banking — help.salesforce.com

Offline Mode — cbtcnet.com

Why SDK.finance Uses Modular Architecture Instead of Microservices — sdk.finance

Best Chatbots in Banking to Transform Services — neontri.com

Using AI and Apps for Personal Finance Automation — banklandmark.com

Top Fintech Integration APIs for Payments, Compliance & Banking — dashdevs.com

Payment Gateway Integration: The Ultimate Guide — appinventiv.com

Core Banking Integration for Financial Modernization — crassula.io

Integrated Banking System: Strategies & Insights — geniusee.com

Mobile Banking App Best Practices for Compliance — guardsquare.com

Cost to Develop a Mobile Banking App — madappgang.com

Cost to Develop a Mobile Banking App — wearetenet.com

Best Practices for Mobile Banking App Security (2025) — codesuite.org

Fintech App Development Cost Factors [2025] — appventurez.com

Regulatory Compliance in App Development — pixelcrayons.com

Fintech App Development Cost in 2025 — stepmediasoftware.com

Critical Security Features for Finance Mobile Apps — thisisglance.com

AI in Banking: Enhancing Revenue & CX — forbes.com

AI’s Impact on the Future of Banking — ascend.bank

AI-Powered Customer Transformation Stories — microsoft.com

What’s Holding Banks Back From AI — forbes.com

AI Gold Rush: Rewriting CX in Digital Banking — theuxda.com

AI in Customer Experience (CX) — ibm.com

Banking App Performance & Testing — qable.io

5 Mobile Banking Apps: 7 Stats Every User Should Know — numberanalytics.com

Mobile Banking Stats by Generation & Usage — mx.com

Cybersecurity in Mobile Finance Apps — nowsecure.com

Mobile Finance App Engagement Stats — storyly.io

Fintech UX Design Importance — goldenflitch.com

User-Centric Interface & UX Impact — medium.com (Pepper Square)

Software Scalability in IT Systems — vaultinum.com

Offline-First Design: Challenges & Solutions — dashdevs.com

What a Scalable Company Is — investopedia.com

5 Key Benefits of Mobile Banking — bankrate.com

Build an Offline-First App (Android Developers Guide) — developer.android.com

Ongoing Maintenance for Mobile Apps — digitaloneagency.com.au